Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The Question Almost Every Buyer Is Asking

If you’ve been thinking about buying a home lately, you’ve probably heard someone say:

“I’m just waiting for rates to get back into the 5s.”

It sounds reasonable. After all, mortgage rates briefly dipped into the upper 5% range twice already this year before moving back into the low 6s.

For many buyers, that moment felt like a missed opportunity.

But here’s the question that rarely gets asked:

Does moving from the low 6s to the high 5s actually change the monthly payment as much as people think it does?

The answer might surprise you.

And if you’re looking to buy in communities like Walpole, Westwood, Dedham, Norfolk, Wrentham, Roslindale, or West Roxbury, understanding this math could help you decide whether waiting really makes sense.

The Payment Difference Isn’t What Most Buyers Expect

Let’s look at a simple example.

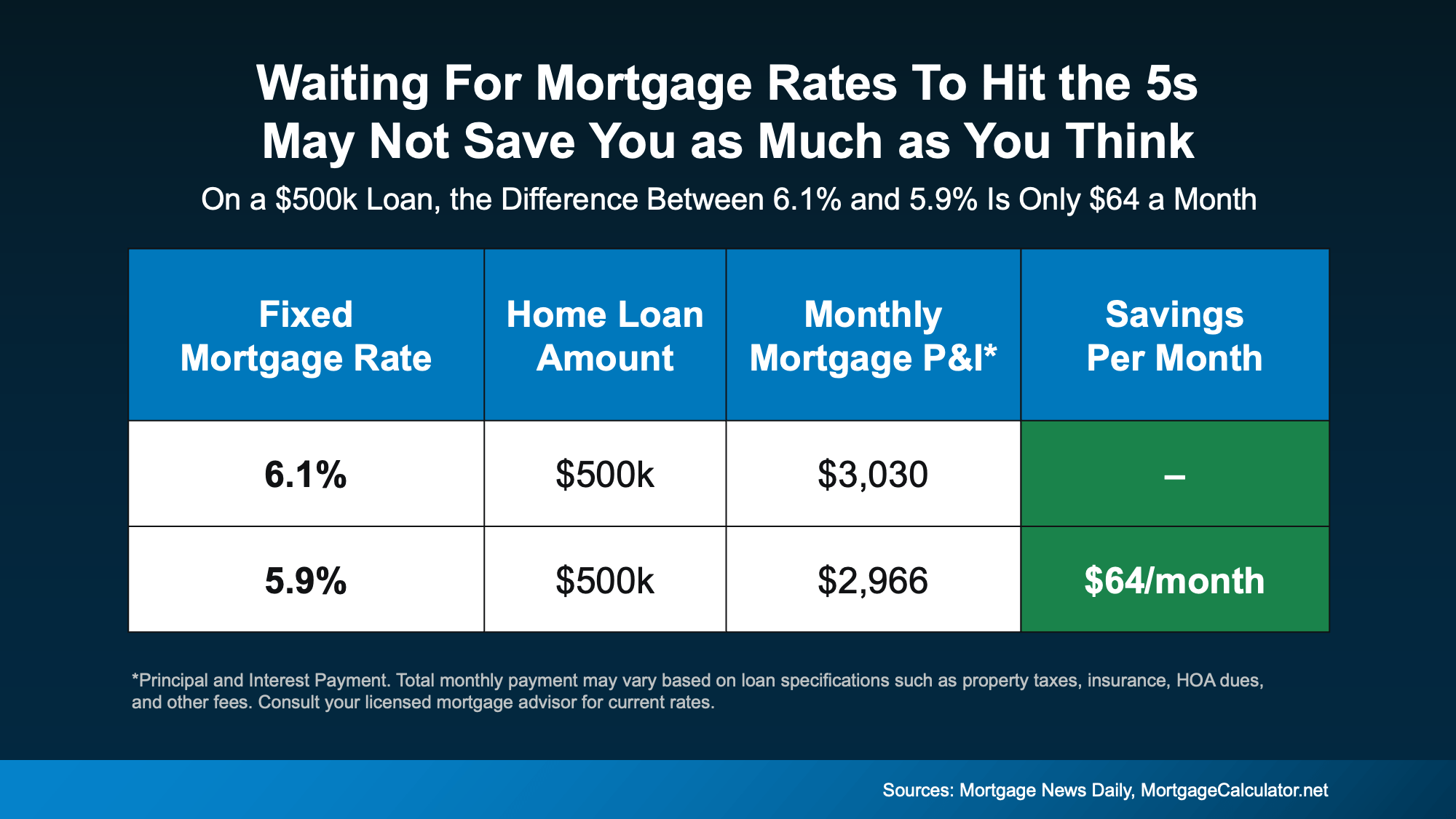

Assume you’re financing a $500,000 home loan.

At 6.1%, the principal and interest payment is roughly $3,030 per month.

At 5.9%, it drops to about $2,966 per month.

That’s a difference of $64 per month.

Not $300.

Not $500.

Just $64.

Yes, over time that $64 adds up.

But it’s far from the dramatic shift many buyers imagine when they say they’re waiting for mortgage rates to start with a “5.”

In many households, $64 is less than the monthly cost of a streaming subscription and dinner takeout.

So while the psychological difference between 6.1% and 5.9% feels big, the actual payment difference is often surprisingly small.

Why the “5% Number” Feels So Important

There’s a reason buyers fixate on mortgage rates beginning with a 5.

It’s largely psychological.

Humans respond strongly to number thresholds.

Just like:

-

$399 feels cheaper than $401

-

A $999 item feels dramatically different than $1,001

-

Gas at $2.99 feels cheaper than $3.01

The same thing happens with mortgage rates.

Seeing 5.99% instead of 6.01% feels like a major milestone.

But financially, the difference between those numbers is often minimal compared to other factors like:

-

Home price

-

Down payment

-

Property taxes

-

Insurance

-

Loan type

Those variables can change your payment far more than a small movement in interest rates.

Experts Aren’t Forecasting a Big Drop

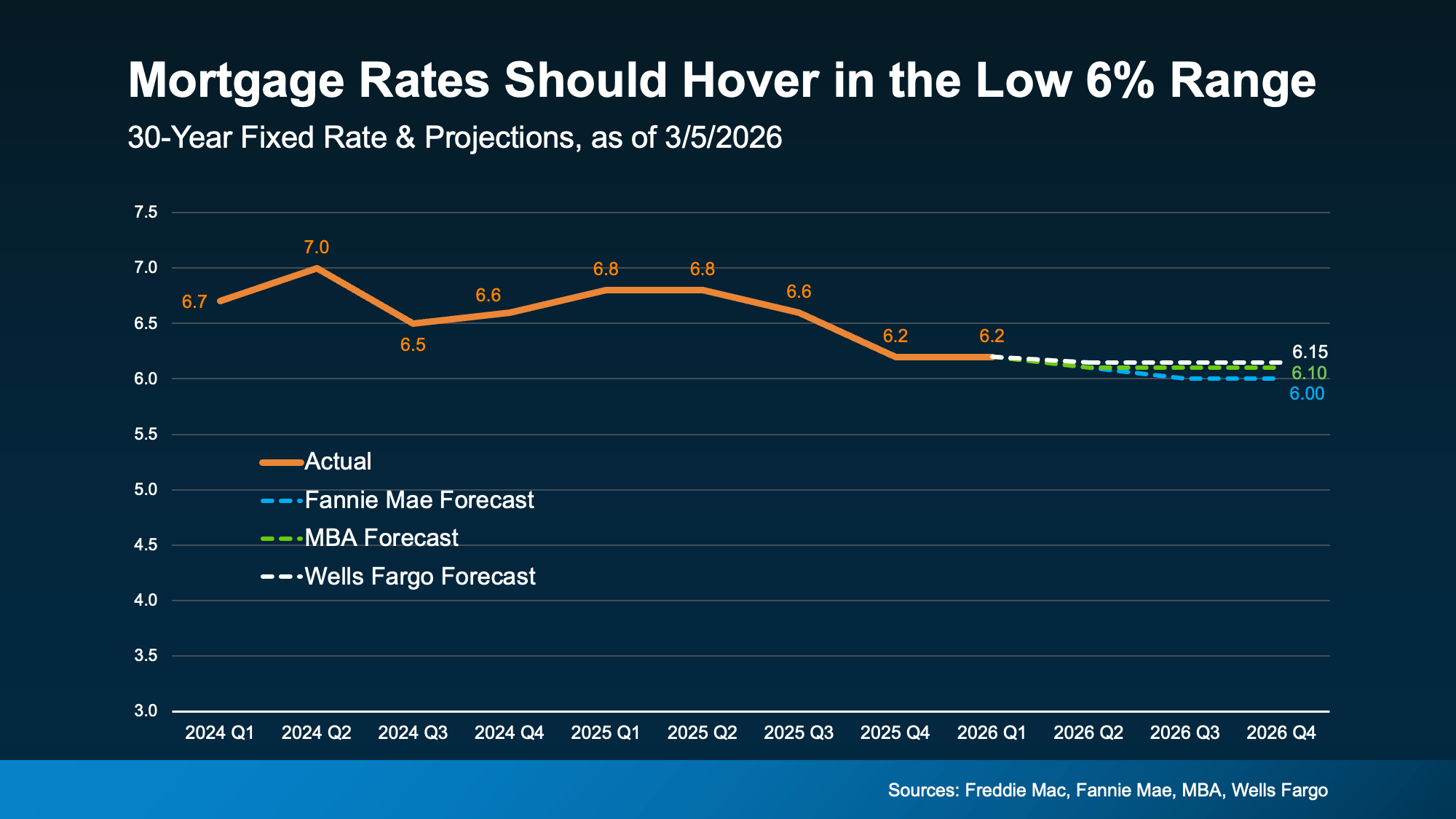

Another important reality to consider is what housing economists are actually predicting.

Right now, many forecasts suggest mortgage rates will hover in the low 6% range through much of the year.

While rates will likely move up and down — occasionally touching the high 5s — most projections don’t expect a sustained return to 5% territory anytime soon.

That means waiting specifically for a large drop in mortgage rates may not deliver the payoff many buyers are hoping for.

And during that waiting period, home prices and competition can continue moving.

The Better Question Buyers Should Ask

Instead of asking:

“Did I miss the moment when rates hit the 5s?”

A more helpful question might be:

“Does today’s payment work comfortably within my budget?”

If the monthly payment works for your financial situation, and you’ve found a home that fits your needs, the difference between 6.1% and 5.9% may not be the deciding factor.

It’s one piece of the puzzle — but not the entire picture.

Remember: Mortgage Rates Aren’t Permanent

Another point many buyers overlook is that mortgage rates today don’t have to be your rate forever.

If rates drop meaningfully in the future, refinancing may become an option.

But you can only refinance a home you already own.

Buyers who delay their purchase waiting for the perfect rate sometimes discover that:

-

Home prices increased

-

Inventory tightened

-

Competition returned

In other words, the opportunity they were waiting for didn’t necessarily create the advantage they expected.

Waiting Might Feel Safe — But It Isn’t Always Strategic

It’s completely understandable to want the best possible rate.

Everyone does.

But buyers sometimes overestimate how much a rate change into the high 5s would actually impact their finances.

What often gets overlooked is that mortgage rates have already improved significantly compared to recent years.

Not long ago, rates were hovering in the 7% range.

Today, they’re sitting much closer to the low 6s, which for many buyers represents a meaningful improvement in monthly affordability.

If you paused your home search when rates were higher, it may be worth running the numbers again.

Not because rates are perfect.

But because the payment math might already work better than you think.

Bottom Line

If you’ve been sitting on the sidelines waiting for that “magic number” mortgage rate, the strategy may not deliver the dramatic savings many buyers expect.

Sometimes the difference between waiting and moving forward comes down to a payment change smaller than most people realize.

Before assuming you missed your opportunity, it may be worth looking at the numbers again.

You might find the opportunity never disappeared.

If you’re thinking about buying, let’s take a quick look at the numbers together.

A simple payment comparison at your price point may show that buying now is more realistic than you expected.

Reach out anytime for a quick home affordability review or to explore available homes in your target area.