Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Think Nobody’s Buying Homes Right Now? Think Again.

If you’ve been thinking about selling, you’ve probably seen plenty of headlines suggesting buyers have just about disappeared. But there’s a big difference between a slow market and a stalled one.

Yes, mortgage rates are still higher than most people would like. Homes aren’t selling as fast as they were. And every week seems to bring another headline about buyers sitting on the sidelines. But here’s what you haven’t heard.

Despite everything going on, buyer demand has been remarkably resilient.

In fact, more sellers are getting to put up the “pending sale” sign now than during the last two years. What’s even more surprising is that they’re doing it at a time of year when activity usually starts to slow down.

And if you’re thinking about selling, that’s a trend worth paying attention to.

Buyers Are More Active Than You Think

One of the best ways to measure buyer demand is by looking at pending home sales. Those are homes that have gone under contract but haven’t closed yet. Think of them as a real-time pulse check on the market and whether buyers are still buying.

HousingWire Data shows more homes are going under contract than at the same time the past 2 years (see graph below):

While it may come as a surprise, the numbers speak for themselves. It doesn’t mean buyers are everywhere, but it does mean they’re still active right now. And even if this ebbs and flows a bit in the weeks ahead, right now we’re still ahead of where we’ve been lately. That’s encouraging news if you’re thinking about selling because it tells us something important…

People haven’t stopped buying homes. Serious buyers are still making moves.

And a lot of these people are buying because they decided they can’t keep waiting. Whether it’s a growing family, a new job, retirement, or simply wanting a different home, life keeps moving… even when mortgage rates stay higher than we’d like. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

“A late spring buyer rush—even with mortgage rates not budging—is an indication of pent-up housing demand and consumers’ acceptance of above-6% mortgage rates as the new normal.”

So, if you’ve been worried no one’s buying, this data should give you some confidence. Today’s buyers aren’t just casually browsing open houses on a Sunday afternoon, they’ve spent months waiting for rates to improve and now they realize they can’t wait anymore.

That means they have a purposeand a timeline. And that’s exactly the kind of motivated buyer you want to work with.

What This Means for Your Sale

Does that mean every house will sell instantly? No.

Today’s market is more balanced than it was a few years ago. So, you can’t just price your house however you want or skip preparing it for the market.

Now buyers have choices, and they’re willing to wait for the right home at the right price. But sellers who understand today’s market (and price and position their homes right) are still finding success. Because the idea that “no one’s buying right now” just isn’t supported by the data.

The buyers are there.

The opportunity is there.

The key is having the right strategy to capture it.

Bottom Line

This year’s housing market may be moving slower than many of us hoped. But, buyer demand is more resilient than the headlines suggest.

If you’re wondering whether there are enough buyers for your house, let’s connect. I’ll show you what’s happening in our local market and build a strategy that helps you take advantage of the momentum that’s already here.

What To Expect from the Housing Market in the Second Half of 2026

If the first half of this year has left you feeling stuck, you’re not the only one. Mortgage rates stayed higher than people wanted. Affordability remained tight. And uncertainty overseas added another layer of pressure nobody saw coming.

That’s why so many people are asking the same question: Will the second half of the year be any better for the housing market?

While nobody has a crystal ball, there are a few encouraging signs things could start moving in a better direction. Here’s what to watch.

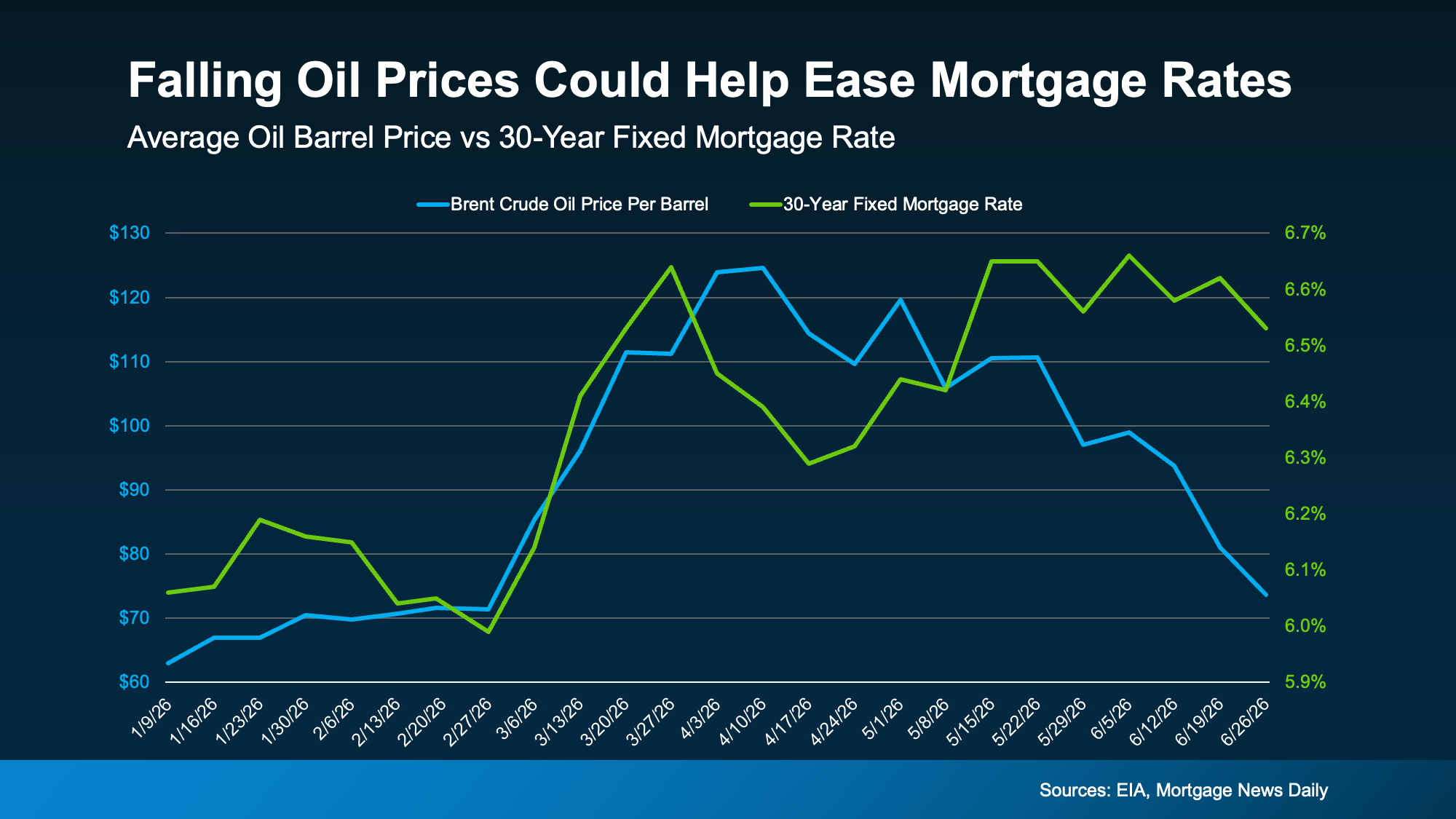

Mortgage Rates Could Be Near a Turning Point

One of the biggest reasons mortgage rates haven’t come down yet is inflation. And higher energy prices and uncertainty overseas are at least part of the reason inflation is still elevated. The encouraging news?

Oil prices have already started coming back down.

That may not sound like it has much to do with buying a home. But historically, mortgage rates and oil prices tend to move in the same direction.

Take a look at the graph below. Generally, they rise and fall together. Both went up in February when the conflict began. While there’s been some volatility lately, experts at the U.S. Energy Information Administration (EIA) say oil prices are forecast to come down. And since oil prices have been on an overall downward trend lately, mortgage rates could come down too:

It’s too soon to say exactly when that will happen (or by how much they’ll fall), but if energy prices go down, inflation cools off, and tensions overseas ease, mortgage rates could come down in the second half of the year.

And that’s good news for anyone thinking about moving. The first half of the year tested everyone’s patience. The second half may finally reward it.

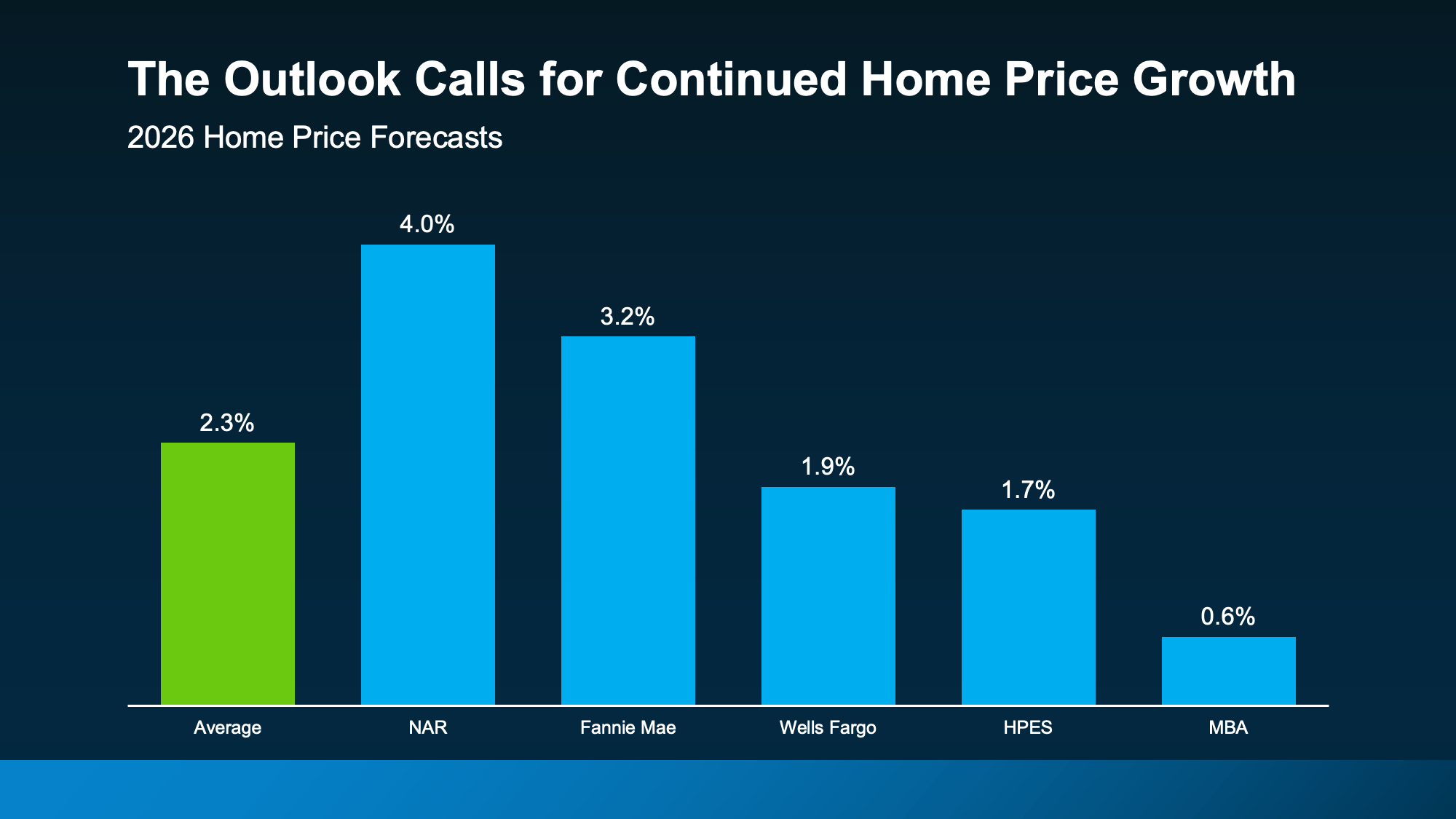

Home Prices Could Pick Back Up

A lot of people want home prices to fall too. But that’s not what most forecasts show.

While price trends are going to vary by area, and some places are seeing mild declines, experts still expect home prices to net positive this year at the national level.

In fact, they’re projecting prices will rise by an average of 2.3% in 2026 (see graph below):

What does that mean for you? Right now, Federal Housing Finance Agency (FHFA)data shows prices are up about 1.7% nationally year-over-year. The average forecast for all of 2026? 2.3%.

Based on those projections, home price growth would have to pick up a bit during the second half of the year. Nothing dramatic, just enough to finish the year around that projected 2.3% gain.

Here’s why that’s possible.

The number of homes for sale has grown, but that growth may be starting to slow down. And if rates improve, more buyers could jump back into the market. More buyers competing could put modest upward pressure on prices, especially if inventory’s not growing as fast.

That’s why buyers shouldn’t assume waiting will guarantee a lower price later. And for sellers, that’s great news if you’ve been worried about your home’s value.

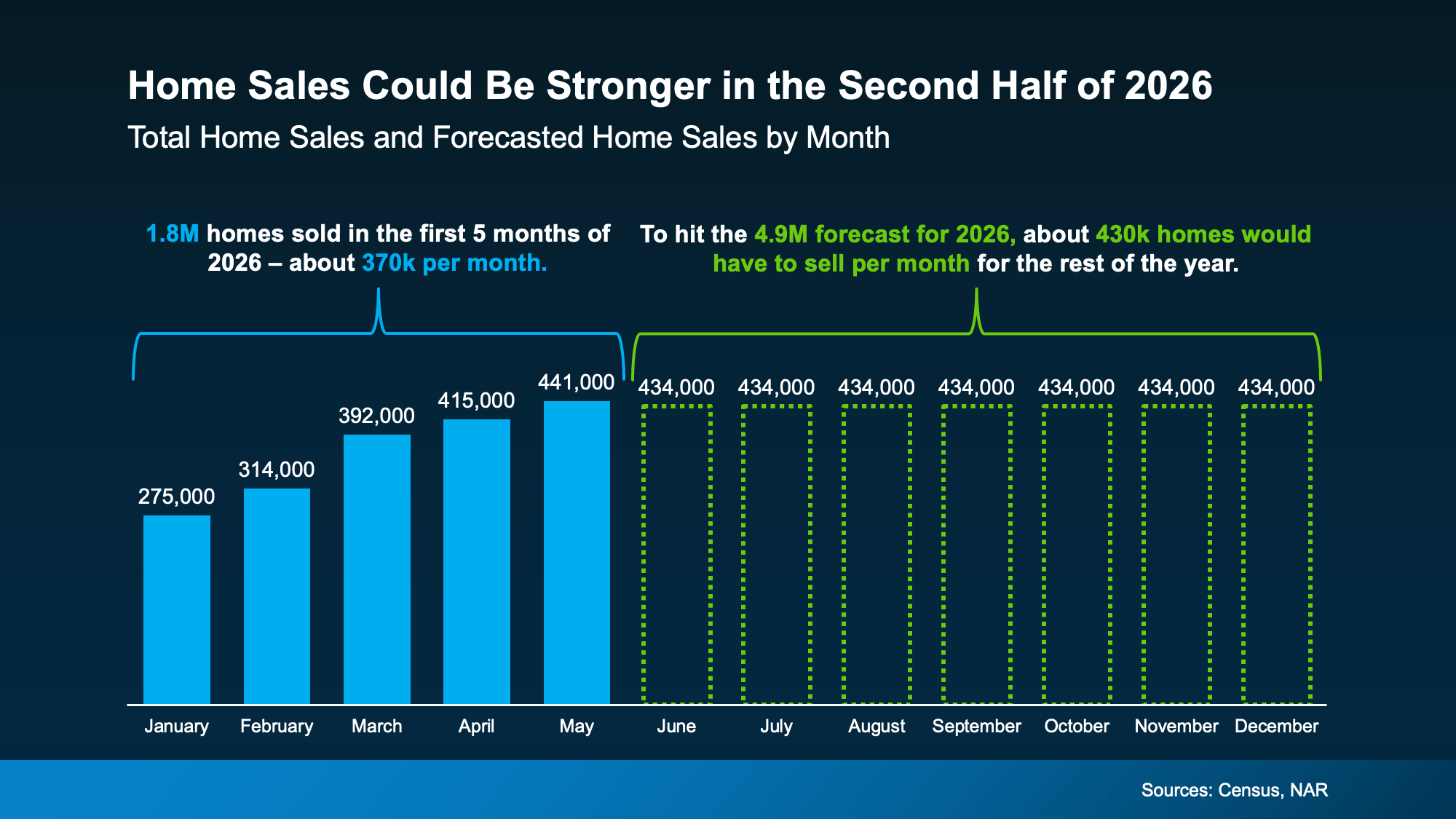

More Homes Are Expected To Sell

If you’ve been wondering why the housing market has felt quieter lately, you’re not imagining it. Home sales have been slower than many experts expected. But that doesn’t mean people have stopped wanting to move.

A lot of people still want or need to make a change. They’ve just been waiting for more certainty, better affordability, or a clearer read on where the market is headed. And early signs show that may be on the horizon.

If rates ease and confidence improves, more people may finally move. As Odeta Kushi, Deputy Chief Economist at First American, explains:

“Overall, we expect pent-up demand to continue emerging gradually. But the pace of recovery will vary significantly across markets and will depend on the path of rates, labor market conditions and inventory growth.”

Based on the latest forecasts, to hit the number of sales expected this year, here’s what would have to happen. The second half of the year would need to outperform the first in sales (see graph below):

In fact, each month for the rest of 2026 would have to come close to matching the best month we’ve had so far this year (May). That’s a sign the experts are calling for more momentum headed into the second half.

More people will finally make their move happen – and you’ve got the chance to be one of them.

Bottom Line

The second half of the year probably won’t be perfect. But it could be better.

Mortgage rates may ease. Home sales could pick up. And prices are expected to continue rising at a healthier, more sustainable pace. If you’ve been waiting for signs of progress, this is it.

If you want to understand what these forecasts mean for your plans and what’s happening in our local market, let’s connect.

That House That’s Been Sitting Could Be Your Best Shot at a Deal

Open up a home search and you’ll see them. Listings that have been on the market for two months. Three. Some longer.

Most buyers scroll right past them, assuming something’s wrong with the house. But that instinct could be costing you, since the longer a home sits, the more motivated the seller usually gets.

Where Some Buyers Are Finding Better Deals

If affordability has been your #1 hurdle to buying, here’s a surprisingly simple strategy that could help you finally get your foot in the door. Start with the homes that have been sitting the longest. That’s often where the best deals are.

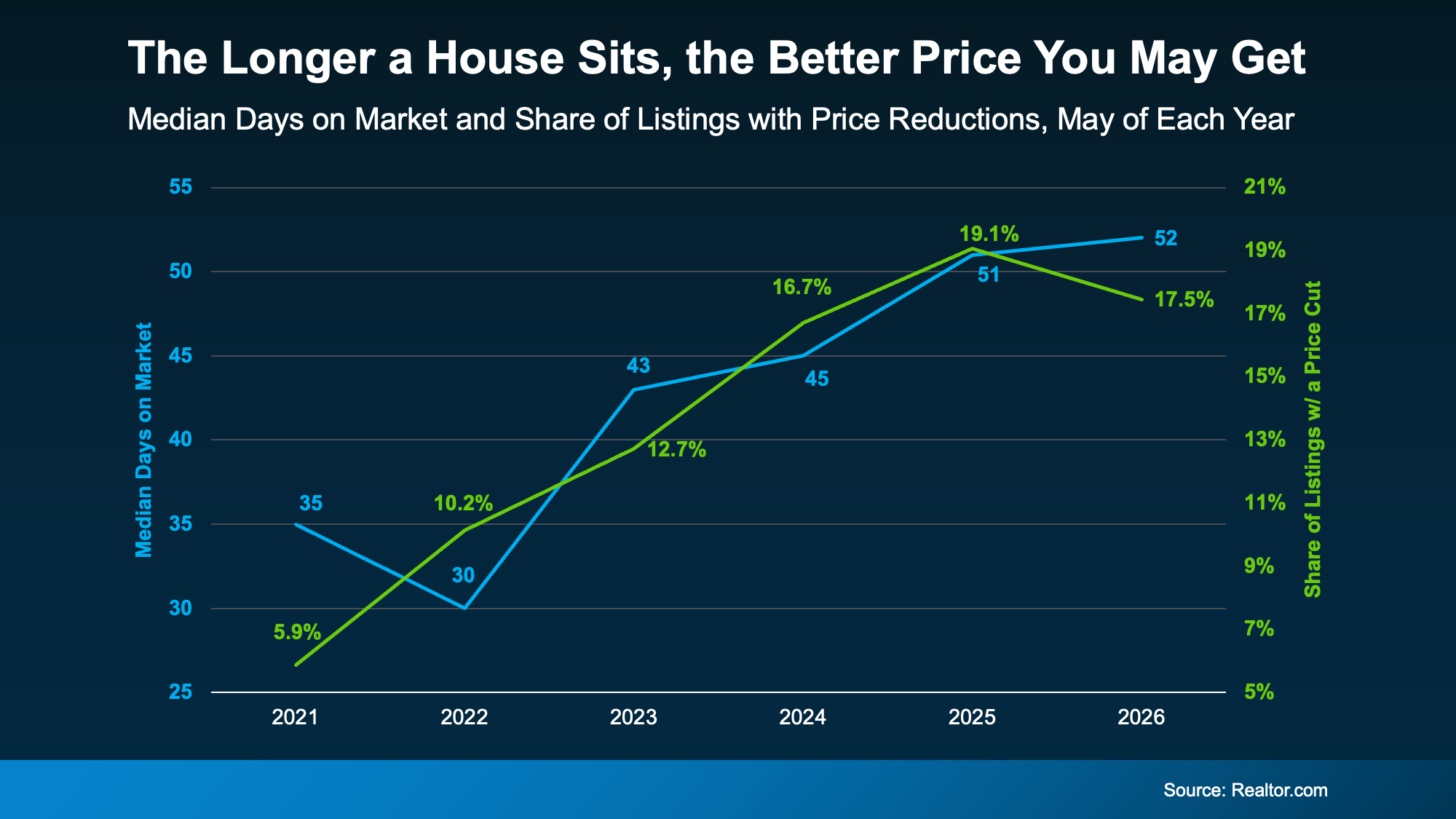

Here’s why. Data from Realtor.com shows there’s a connection between longer time on the market and lower sales prices. Basically, the longer a house sits, the more likely it is that the seller will reduce the price (see graph below):

The blue line tracks how long homes stay on the market, while the green line tracks the share of homes getting a price reduction. As one climbs, so does the other.

And if you focus on these homes that are just sitting and waiting, the opportunity for you is bigger than you may think right now.

Redfin data shows there’s $347 billion worth of stale listings on the market right now – more than ever before for this time of year. So, ask your agent to filter listings for you from oldest to newest. The home that fits your budget might already be there. Just further down the list than you thought.

Lingering Doesn’t Always Mean Something’s Wrong

Let’s say you do that and something catches your eye. Still, you might be questioning why the home has been sitting in the first place. Just remember, sometimes it has nothing to do with the home itself.

According to Redfin, common causes are:

- The asking price was set too high to start

- The home didn’t show well online

- There are a lot of homes for sale in the area, so it just got buried

So, nothing that’s necessarily a dealbreaker, or even anything that’s wrong with the home itself. If there’s a real issue, a thorough inspection will surface it. And that’s information you can use to negotiate. Not a reason to assume it’s a house worth skipping over.

How To Turn a Lingering Listing into a Win

So how do you capitalize on a lingering listing? According to USA Today, you have two main levers to pull.

The first is price. Work with your agent to study what comparable homes recently sold for, then build an offer around that. Coming in below asking price is fair game when a home has been sitting.

The second is concessions. If a seller won’t budge much on price, they may still help in other ways, like covering some closing costs, repair credits, or even a mortgage rate buydown that lowers your monthly payment.

A local agent has the context to tell which homes are the real opportunities and which are skippable.

Bottom Line

A house sitting on the market isn’t always a glaring red flag. In today’s market, it may be your best opportunity yet.

For help deciding which lingering listings are actually worth a second look, let’s connect.

The Housing Market Is Stronger Than You Think

You’ve probably heard plenty of doom and gloom about the housing market lately. High rates. Stretched budgets. Headlines that make buying or selling sound like a terrible idea. But the data tells a very different story.

This isn’t 2020 or 2021. It was never going to be. Those were the “unicorn years” – historic low mortgage rates, bidding wars on everything, homes flying off the market in days. That kind of market was a once-in-a-generation anomaly, not a baseline. So, when people compare today to that, of course it looks rough.

But compared to almost any other housing market in modern history? This one is holding up remarkably well.

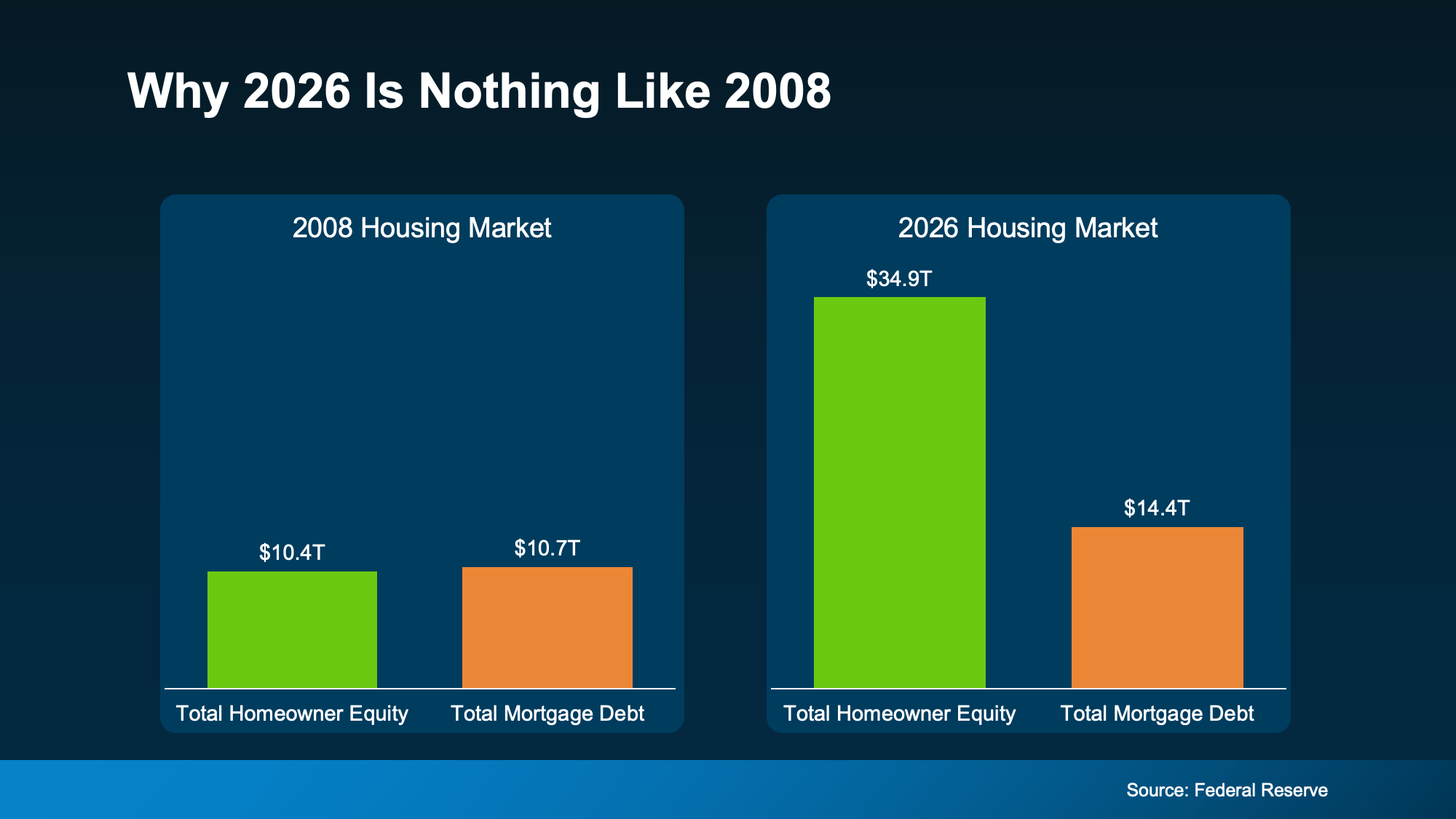

Homeowners Are Sitting on a Mountain of Equity

One of the biggest reasons this market hasn’t cracked is the financial strength of the American homeowner. According to Federal Reserve data, homeowner equity and mortgage debt were nearly identical in 2008. That means, if someone hit a rough patch, they had almost nothing to fall back on. That’s what made that crash so bad.

Today? Total homeowner equity across the country sits at $35 trillion – dwarfing total mortgage debt (see graph below):

That gap means most homeowners aren’t stretched thin or one bad month away from trouble. They own a meaningful chunk of their home and that gives them options. If they needed to sell, many could because they have a cushion. And that cushion grows over time.

That gap means most homeowners aren’t stretched thin or one bad month away from trouble. They own a meaningful chunk of their home and that gives them options. If they needed to sell, many could because they have a cushion. And that cushion grows over time.

- Realtor.com found that homeowners who’ve been in their home just 5 years have built up around $180,000 in equity on average. Stick around 6-10 years, and that jumps to over $340,000.

- Data from ATTOM and the Census shows two-thirds of homeowners either own their home outright or have more than 50% equity.

That’s not a fragile market. That’s a population of homeowners who are financially positioned to sell, to stay, or to make their next move from a place of strength rather than pressure.

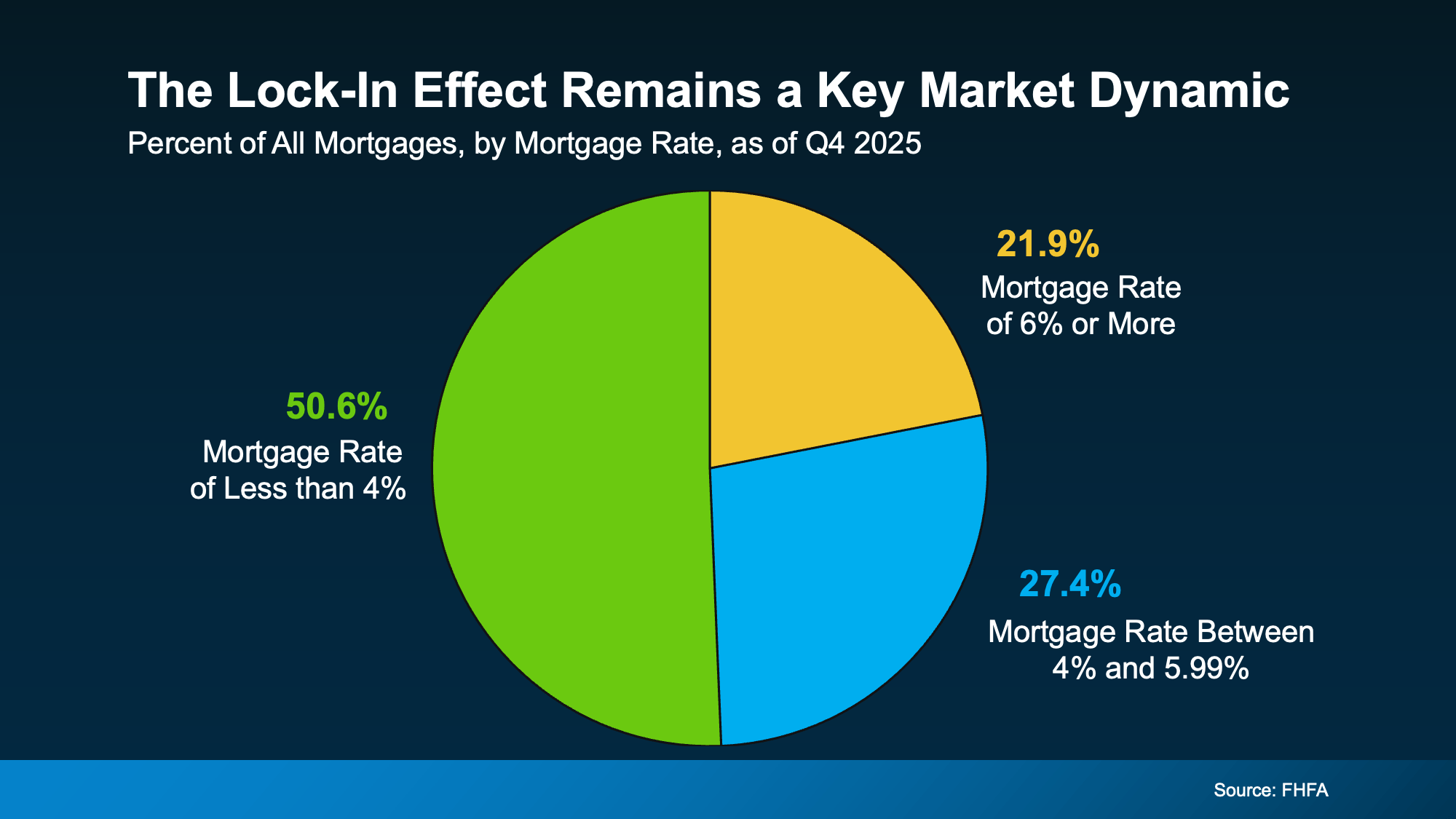

Low Rates and Low Foreclosures

At the same time, Federal Housing Finance Agency (FHFA) data shows more than half of all active mortgages still carry a rate below 4% (see graph below):

That’s a big reason inventory stays tight. Those homeowners aren’t in a rush to trade their rate for a higher one. They’re sitting comfortably in a strong financial position, not scrambling.

That’s a big reason inventory stays tight. Those homeowners aren’t in a rush to trade their rate for a higher one. They’re sitting comfortably in a strong financial position, not scrambling.

That comfort shows up in the foreclosure numbers, too. Despite a slight recent uptick, foreclosure volumes remain dramatically below historical norms, according to ATTOM. Homeowners aren’t losing their homes in droves. They have equity, they have breathing room, and most have options that keep them out of financial distress.

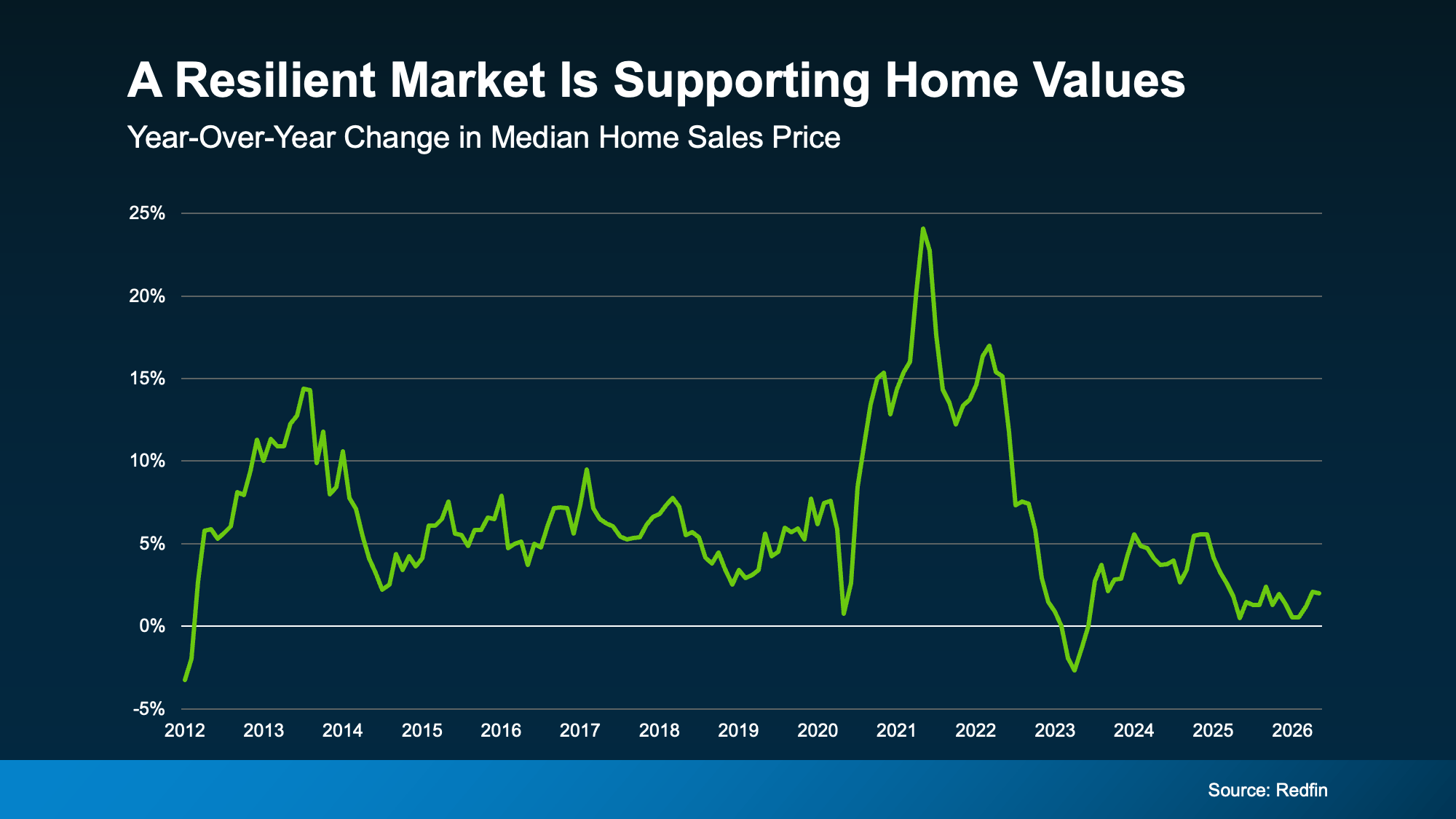

Prices Are Stabilizing, Not Crashing

Here’s another point on the resilience of the market. Redfin research shows home prices are still rising, but the pace has slowed, now closer to 2% year-over-year nationally (see graph below):

That slowdown is good news, as Daryl Fairweather, Chief Economist at Redfin, explains:

That slowdown is good news, as Daryl Fairweather, Chief Economist at Redfin, explains:

“We’re in the middle of a long-term housing market correction, not a housing market crash. After the pandemic-era frenzy sent prices soaring and inventory to historic lows, the market needed a reset.”

Bottom Line

This market isn’t broken, and waiting for a crash that isn’t coming has a cost. Every month spent on the sidelines is a month someone else is building equity, locking in a price, or getting ahead of what most experts expect to be a housing surge once broader economic conditions settle.

Whether you’re thinking about buying or selling, a local real estate agent can help you figure out what this market means for your specific situation and what your next move could look like.

The Pricing Mistake That Could Cost You Your Sale

Most sellers come into the market with one number in mind. And it’s often the one that costs them the most. That’s their asking price.

A survey from Realtor.com shows about 8 in 10 (80%) of sellers expect to sell at or above their asking price today. But here’s where things get interesting.

In reality, only about 4 out of every 10 (roughly 40%) actually do.

That’s a big gap. And it’s where a lot of sellers get caught off guard. So, why the disconnect? And how can you set yourself up to be one of the 4 in 10 that get top dollar?

Let’s break it down.

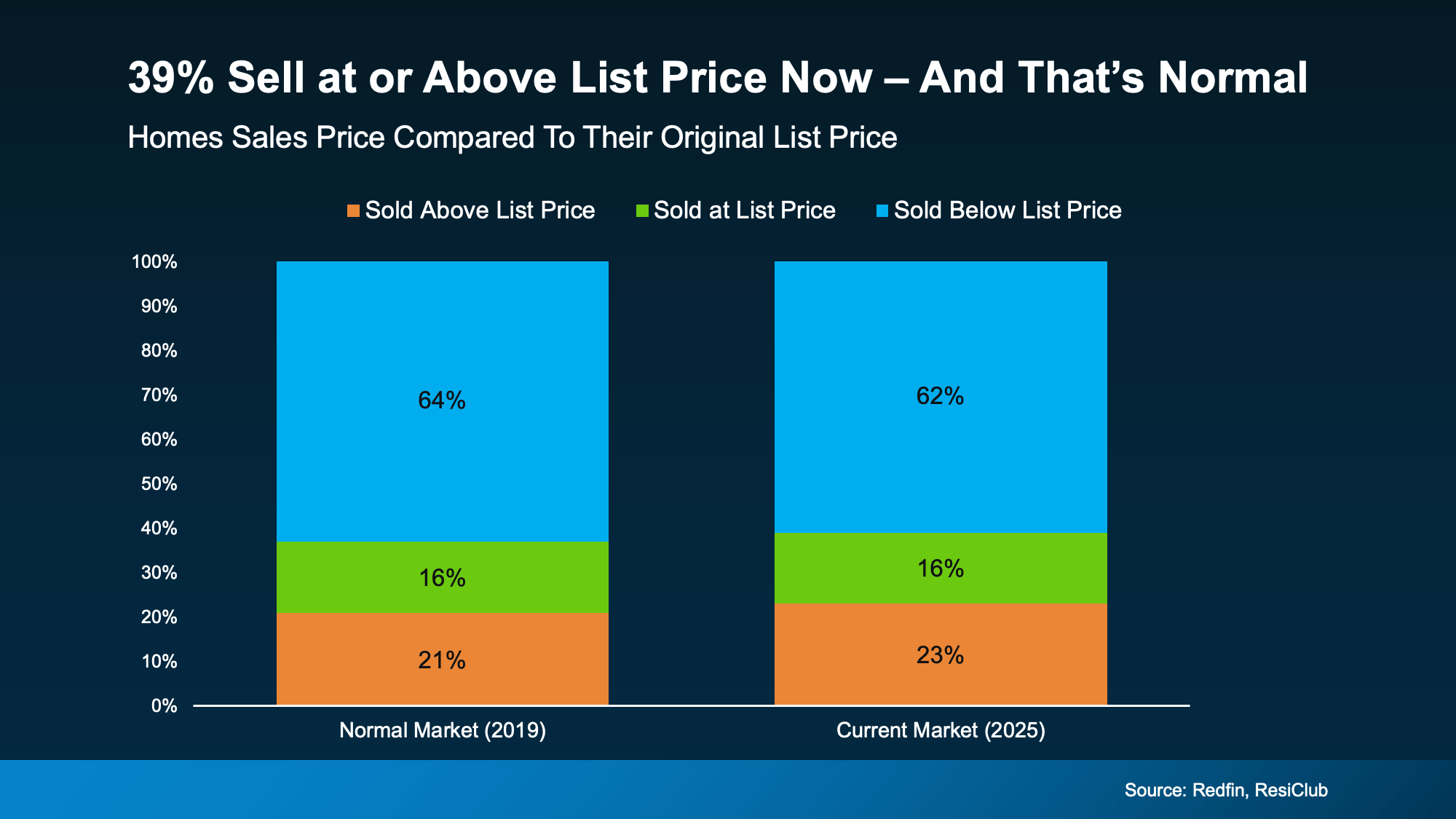

What Should You Really Expect To Get for Your House?

That 40% may sound low at first, but it’s not.

If you look back to the last typical year for the housing market (2019), what we’re really seeing is a return to what’s normal (see chart below). If anything, slightly more homeowners are able to sell above list price today compared to 2019:

It only feels low because the past few years were anything but typical. Between 2020 and mid-2022, buyer demand was sky-high and the number of homes for sale was at record lows. Almost everything sold over asking.

It only feels low because the past few years were anything but typical. Between 2020 and mid-2022, buyer demand was sky-high and the number of homes for sale was at record lows. Almost everything sold over asking.

Now, the market has shifted.

There are more homes for sale. Buyers have more options. And that means they’re more selective about how they spend their money.

In other words, the rules have changed – and pricing like it’s still 2021 is where sellers run into trouble. You have to meet the market where it is if you really want to cash in big.

What Happens When a Home Is Priced Too High

Here’s the reality. It’s easy to think pricing high gives you room to negotiate. But it usually does the opposite.

When your home is priced above what buyers expect, in this market, they don’t negotiate. They move on.

Because buyers notice price first. And if your home doesn’t line up with similar options in your area, it may not even get a showing. And that’s when things start to snowball:

- A high price gets less interest from buyers.

- Less interest means fewer offers.

- And fewer offers usually means more time on the market.

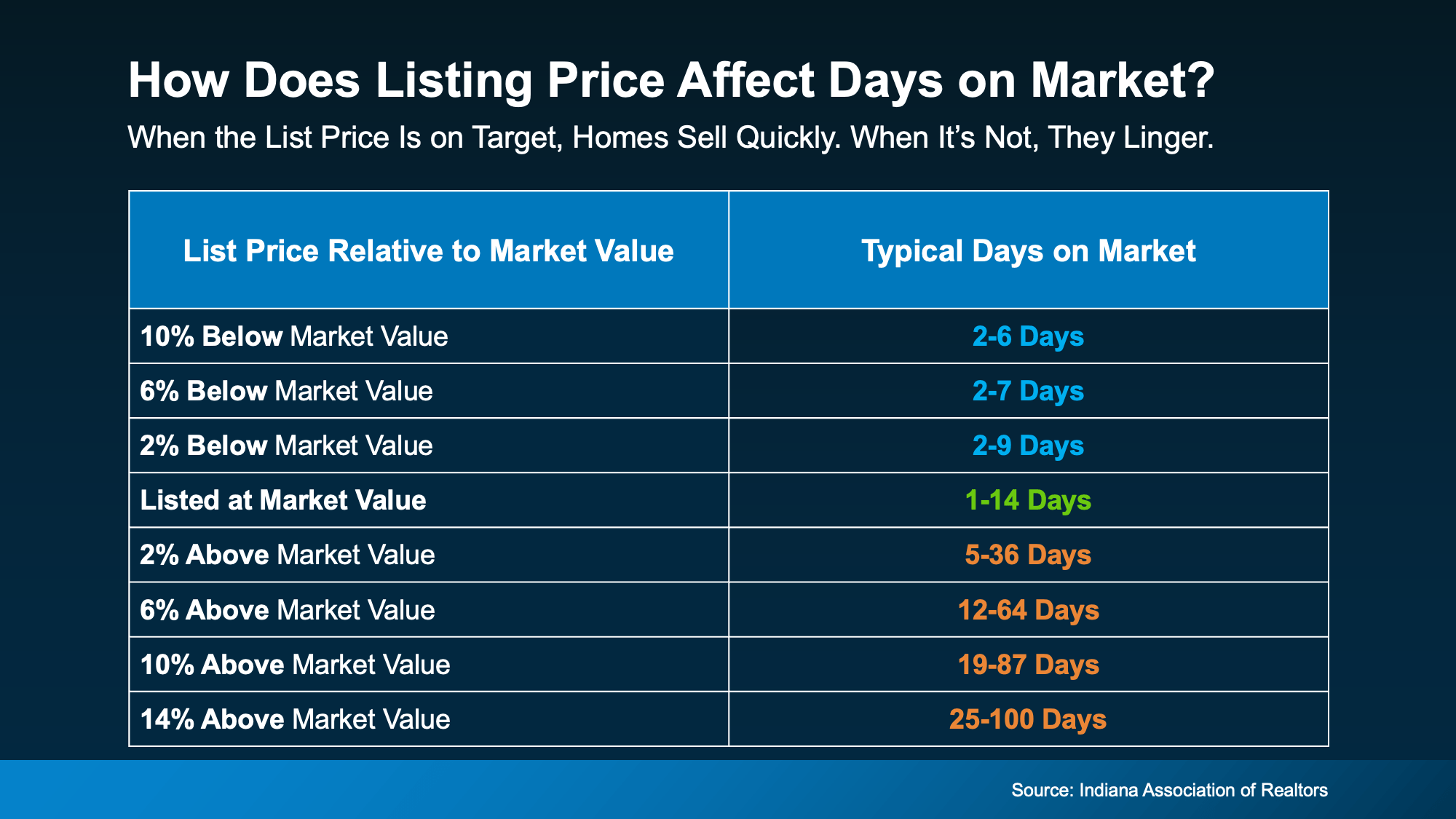

Take a look at this table from the Indiana Association of Realtors. While this data is from one state, the general trend is going to hold true across many markets in the country. It shows that homes listed at or under market value sell fast. But homes priced high? They linger. And that delay comes at a very real cost.

The Price Cut Trap (And How To Avoid It)

The Price Cut Trap (And How To Avoid It)

The Price Cut Trap (And How To Avoid It)

The Price Cut Trap (And How To Avoid It)When a home sits that long without offers, a lot of sellers will do a price reduction. According to Realtor.com, 16.7% of sellers are going that route today.

But here’s the real problem. Even a price cut doesn’t guarantee a sale.

In fact, some buyers will see a reduction as a sign something’s wrong with the house – even when nothing is.

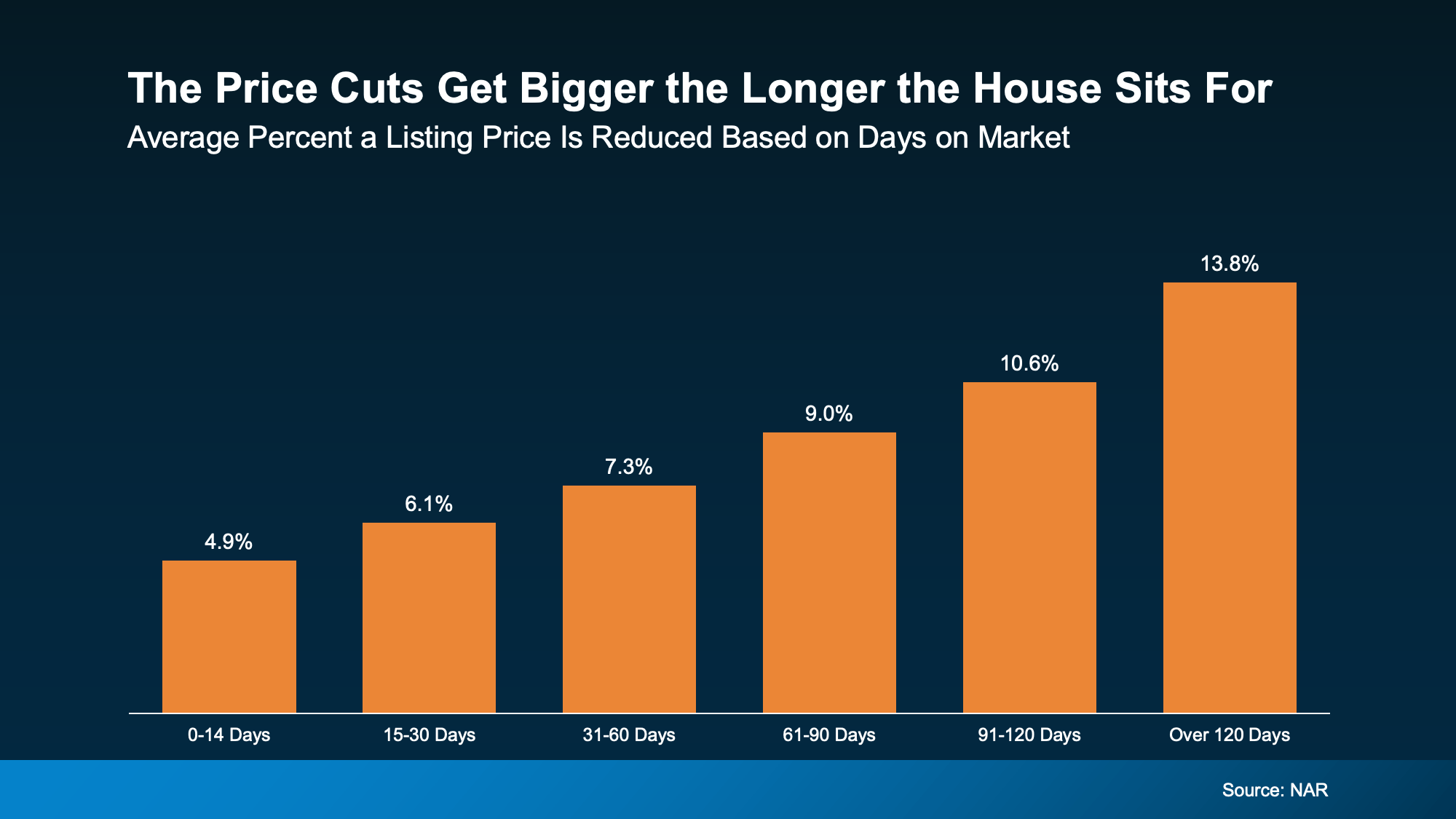

That’s why data from the National Association of Realtors (NAR) shows the longer a home sits, the bigger that price cut tends to be to attract buyers back:

So, what starts as a strategy to “leave room” for negotiate can end up costing you more in the long run.

So, what starts as a strategy to “leave room” for negotiate can end up costing you more in the long run.

Why Pricing Right from Day One Matters

Even though listing at or even just shy of market value may sound counter intuitive if you’re looking to get as much money for your house as possible, a lot of the time it really is the best strategy.

Because the goal isn’t just to list your house to see what price sticks. It’s to price it in a way that creates demand from day one.

NAR puts it best:

“While some sellers are pricing their homes higher than ever, a more ‘goldilocks’ frame of mind is a better approach to avoid price cuts and lingering time on the market.”

In other words, there’s a sweet spot. Too high, and buyers disappear. Too low, and they question the value.

But right in the middle? That’s where the magic happens.

And that’s where the right agent comes in.

They help you understand what buyers are actually paying right now, how your home compares, and how to price it so it stands out immediately. And in today’s market, that strategy is the difference between:

- Listing high, watching it sit, and selling for less later.

- Or, pricing it right, creating competition, and putting yourself in a position to win from the start.

Bottom Line

A lot of homeowners think they can list high now and negotiate later, but that’s a mistake that costs them. And it’s the reason only 4 out of every 10 sellers are getting their asking price or more.

If you want to be in that group, it starts with getting the price right from day one.

Let’s connect so we can make sure you are.

Reverse Mortgages Explained: What Homeowners Should Know Before Tapping Into Home Equity

For many older homeowners, the house is more than a place to live. It is also one of their largest financial assets. After years of mortgage payments, repairs, paint colors that seemed like a good idea at the time, and maybe a few questionable wallpaper choices, there may be significant equity built up in the home.

That equity can create options. One of those options is a reverse mortgage.

A reverse mortgage can allow eligible homeowners to access some of their home equity without selling the property or making monthly mortgage payments. But it is not a simple “free money from the house” situation. Like most things involving real estate, lending, and family expectations, the fine print matters.

What Is a Reverse Mortgage?

Unlike a traditional mortgage, where you make payments to the lender, a reverse mortgage works in the opposite direction. The lender pays you, using your home equity as the source of the loan.

The most common type is a Home Equity Conversion Mortgage, often called a HECM, which is insured by the Federal Housing Administration. To qualify for a HECM, borrowers generally must be at least 62 years old, live in the home as their primary residence, and meet other requirements, including counseling through a HUD-approved counselor.

The amount you may be able to borrow depends on several factors, including your age, your home’s value, current interest rates, and how much equity you have. In simple terms, equity is the difference between what your home is worth and what you still owe.

For example, if your home is worth $410,000 and you owe $210,000, you have about $200,000 in equity.

How Do You Receive the Money?

With a reverse mortgage, you may be able to receive funds in a few different ways:

- A lump sum

- Monthly payments

- A line of credit

- A combination of options

That flexibility is one reason reverse mortgages can appeal to homeowners who want to age in place but need more cash flow for expenses, home repairs, medical costs, or general retirement planning.

In areas like Walpole, West Roxbury, Roslindale, Dedham, Norfolk, Wrentham, and Westwood, many longtime homeowners have seen property values rise significantly over the years. That can mean a lot of equity is sitting inside the home — useful, but not exactly easy to spend at the grocery store.

When Does the Loan Have To Be Repaid?

A reverse mortgage does not usually need to be repaid until the borrower passes away, sells the home, refinances, or permanently moves out.

That last part is important.

If the goal is to stay in the home long-term, a reverse mortgage may seem attractive. But if there is a chance you may need to move to assisted living, downsize, or relocate closer to family, the timing and repayment rules matter.

The Big Question: What Happens to the Home?

This is where families really need to pay attention.

When the loan becomes due, the reverse mortgage must be repaid before the home can fully pass to heirs. In many cases, heirs sell the home and use the proceeds to pay off the loan.

If heirs want to keep the home, they generally need to repay either the full loan balance or 95% of the home’s appraised value, whichever is less, for a HECM loan.

That can be a major issue if adult children or other loved ones expected to inherit the property but do not have the funds to pay off the reverse mortgage.

When a Reverse Mortgage May Make Sense

A reverse mortgage may be worth exploring if:

- You are 62 or older

- You plan to stay in the home long-term

- You have substantial equity

- You need additional income or financial flexibility

- You are not strongly focused on leaving the home itself to heirs

- You understand the costs, risks, and repayment rules

For some homeowners, especially those who do not have children or do not expect family members to keep the property, a reverse mortgage may provide breathing room.

When To Be Careful

A reverse mortgage may be less ideal if:

- You want your heirs to keep the home

- A spouse or family member lives there but is not protected under the loan

- You may need to move soon

- You are already struggling with taxes, insurance, or maintenance

- You do not fully understand the long-term impact

This is not a decision to make after one phone call, one commercial, or one enthusiastic brochure featuring suspiciously happy retirees on a beach.

The Bottom Line

A reverse mortgage can be a helpful tool, but it is also a complicated loan product with long-term consequences. Before making a decision, speak with a qualified mortgage professional, a financial advisor, and, if heirs are involved, have a family conversation sooner rather than later.

Your home may be part of your retirement strategy. It may also be part of your family legacy. The right answer depends on your goals, your finances, and what you want the next chapter to look like.

More Options Are Popping Up This Spring

Did you try to buy a home last year, but you ended up pressing pause?

Maybe you couldn’t find a home that really fit your needs. Or maybe the ones you liked just weren’t affordable. According to a recent survey from NerdWallet, those were the top two reasons buyers gave up on their search in 2025.

But this Spring, there’s one trend that could help fix both of those frustration points: more homes are hitting the market.

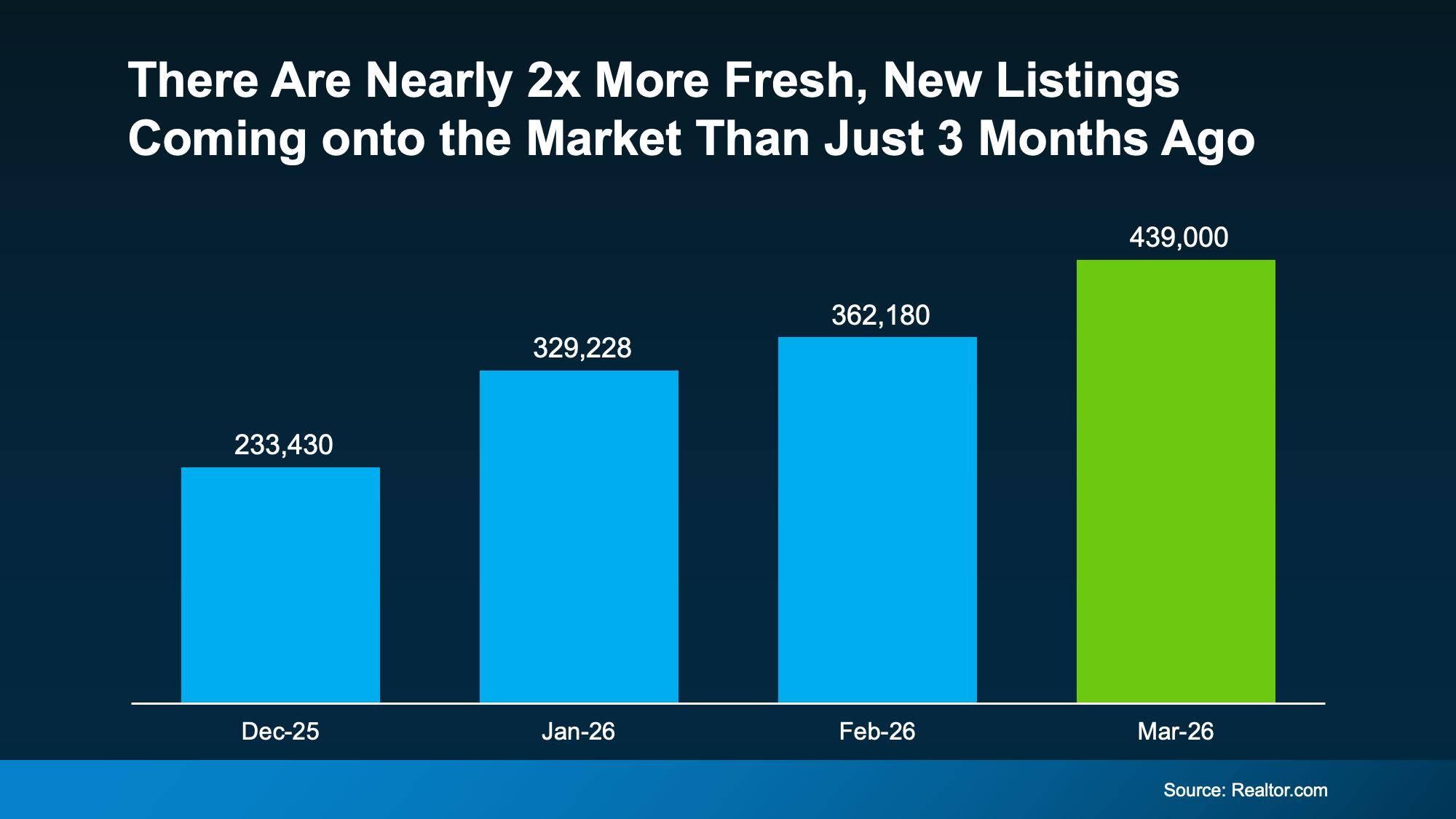

The Number of Fresh Listings Is Almost 2x Higher Than a Few Months Ago

Data from Realtor.com shows there are nearly 2x as many new listings hitting the market today as there were just 3 months ago. Those are homes the seller just put up for sale (see graph below):

That’s a significant rise. And while we usually see an uptick as we head into the busiest time of the year, this increase was bigger than normal. Jake Krimmel, Senior Economist at Realtor.com, explains:

That’s a significant rise. And while we usually see an uptick as we head into the busiest time of the year, this increase was bigger than normal. Jake Krimmel, Senior Economist at Realtor.com, explains:

“New listings jumped 21.2% from February to 439,000, a larger-than-typical seasonal surge . . . March typically sees the biggest month-over-month jump in new listings of the entire buying season, averaging an 18% increase since 2017; this year it exceeded 20%.”

That means more sellers are jumping back into the market, and that’s giving buyers more fresh options to choose from. So, if you’d felt like you’d seen everything out there and still nothing was quite right, this may be your moment.

With that many “just listed” homes, one of them could be exactly what you’ve been searching for.

Where You Have More Options

And this trend is happening across most of the country, so you should have more options pretty much whereever you are.

Earlier this year, the Northeast had fewer new listings because winter storms delayed sellers from putting their homes on the market. But now, that region is catching up fast.

In March, new listings jumped across nearly every state, especially in the Northeast, helping drive a strong national rebound.

What Rising Inventory Means for You

Right now, there are almost a million homes for sale nationwide. That’s up over 8% compared to last year.

With that many homes on the market, there’s a much better chance something will fit what you’re looking for, especially with so many fresh options being added right now. As Odeta Kushi, Deputy Chief Economist at First American, explains:

“One of the most encouraging signals heading into the spring home-buying season is the improvement in for-sale inventory levels compared with last year. . . More homes on the market give buyers greater choice and, combined with improved buying power, expand the range of homes they can realistically consider.”

In other words, your search may feel very different this year.

Bottom Line

More fresh listings are hitting the market right now, and that’s creating real opportunity.

If you put your search on hold last year, this Spring may be the time to jump back in. Let’s take a look at what just hit the market and see what could work for you.

3 Must-Do’s for First-Time Home Buyers

Buying your first home is exciting, but it can also be a little nerve-wrecking because it’s something you’ve never done before. And trying to think of everything you need to do can feel like a lot. But here’s the key.

You don’t have to figure everything out on your own. And you don’t have to do it all at once. Just tackle it one thing at a time.

Here’s a simple list of 3 main things you should focus on to help you get started.

1. Assemble Your Team: Don’t Do This Alone

Buying a home is a team sport. And having the right professionals by your side can make a world of difference. Here’s who you need to find:

- A local real estate agent is your guide from the first showing to closing day. They’ll make sure you understand all the details along the way, so you feel confident in your decision.

- A trusted lender will walk you through loan options, monthly payments, and what’s realistic for your situation. That information is something you’re going to want early on.

2. Prep Your Finances: Set the Foundation First

This is what determines what you can afford, how competitive you’ll be, and how confident you’ll feel when it’s time to make an offer. Here’s how to get ready:

- Check your credit score. Your credit score impacts the loan options you’ll qualify for and even the mortgage rate you’ll get. Knowing this number early gives you time to work on raising your score, if you want to.

- Save for your down payment and closing costs. Most buyers focus on the down payment, but closing costs matter too. Having savings set aside for both helps you avoid last-minute stress and surprises.

- Look into assistance programs. Many first-time buyers qualify for programs that’ll give their homebuying savings a boost. This can make buying possible sooner than you expect.

- Talk to a lender about mortgage options. Fixed-rate, adjustable-rate, FHA, VA, and conventional loans all work differently. Understanding the options helps you choose what fits your goals best.

- Get pre-approved. A pre-approval tells you what a lender would be willing to give you for your home loan. This’ll help you figure out your price range and set you up to move fast when the right home comes along.

- Figure out your budget. Your mortgage is just one part of homeownership. Budgeting for your utilities, home insurance, and everyday expenses and maintenance will help make sure your payment feels comfortable, not stressful.

3. Gather Your Documents: Save Time (and Stress)

When you’re officially ready to kick off the buying process, lenders are going to need to verify your income, assets, and financial history. Having these documents ready-to-go upfront can speed up the process and reduce back-and-forth. Here’s what Bankrate says you need to prep:

- W-2s and tax documents (past 2 years). These show income stability and help

- Recent pay stubs (generally the past 1–2 months). Pay stubs confirm your current income and employment status.

- Bank statements (past 2–3 months). These show your savings, spending patterns, and where your down payment funds are coming from.

- Investment account statements (past 2-3 months). If you’re using investments as part of your financial picture, lenders may ask for these as well.

- Copy of your driver’s license. This verifies your identity and is required for loan processing.

- Residential history (past 2 years). Lenders use this to confirm stability and background information.

- Statements for any outstanding debts (past 2 months). Student loans, auto loans, and credit cards affect your debt-to-income ratio, so lenders will want to know about them.

- Proof of supplemental income. Bonuses, commissions, side work, or child support may count toward your income if documented properly.

Note: the exact time frames and list of documents may vary lender to lender. This is just a general rule of thumb to help you get the ball rolling.

Bottom Line

Buying your first home doesn’t mean you have to have everything figured out. It just requires a plan.

If you start with your finances, organize your documents, and surround yourself with the right people, you’ll be in great shape when the time comes to make a move.

And if you want more information on anything in this list or just need help getting started, don’t hesitate to reach out.

The #1 Reason Buyers Walk Away (And How Sellers Can Stay Ahead)

You may have seen headlines on social saying the number of buyers backing out of their contracts is on the rise – and has recently reached a high not seen since 2017. That can sound intimidating. But it varies a lot by market.

And here’s the key thing to understand if you want to sell. A lot of the time, there’s one common cause. And it’s something you can actually control.

Here’s what you can do to get ahead of the biggest dealbreaker before it ever becomes a problem.

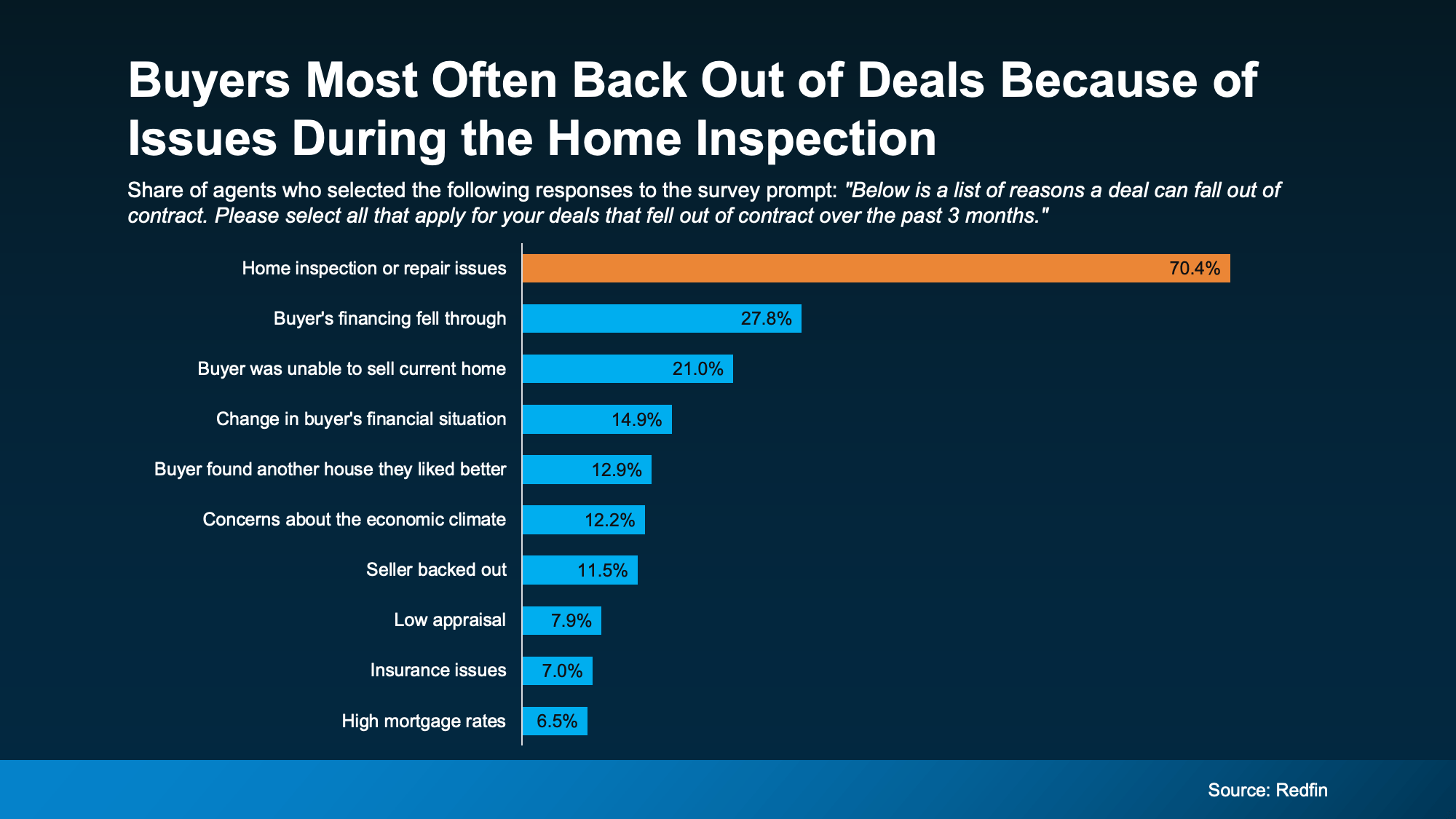

The Top Dealbreaker: Issues That Pop Up During the Inspection

A Redfin survey shows over 70% of recently cancelled contracts happened because of issues during the home inspection (see graph below):

And that makes sense. Because today’s buyers have something they didn’t have a couple of years ago: options.

And that makes sense. Because today’s buyers have something they didn’t have a couple of years ago: options.

Why Fixing Things Before You List Matters More Today

A few years back, when buyers felt rushed or boxed in due to the limited number of homes for sale, they were more willing to overlook issues.

But in today’s market, skipping essential repairs is one of the fastest ways to lose a deal.

Now that there are more homes to choose from, buyers can be more selective. If a house feels risky, outdated, or like it’s hiding expensive surprises, they’re a lot more likely to walk away. So, what do you have to fix? Just ask an agent.

How Your Agent Can Help Give You the Edge

A local agent will be able to walk through your house and offer advice on what to tackle based on your specific home, your market, and what buyers are prioritizing in your area. They’ll also have first-hand knowledge about some of the biggest turnoffs for buyers today. And you can use that expertise to prevent future headaches.

For example, according to Zillow, these are some of the issues buyers will care the most about:

- Roof leaks or damage: sagging, leaking, etc.

- Plumbing problems: standing water, leaks, water damage, etc.

- Electrical concerns: outdated or exposed wiring, missing GFCI outlets, etc.

- HVAC issues: non-functioning units

- Pest or insect damage: termite colonies, etc.

- Hazardous materials: lead, mold, asbestos, etc.

- Safety/code violations: missing smoke detectors, windows stuck closed, etc.

- Structural problems: cracks in the foundation, sagging floors, etc.

Odds are not all of this even applies to your house. Maybe only 1-2 things do. Or maybe none of them do. It just depends. But an agent will have the tools and resources to help you figure it out and stay one step ahead.

The Benefits of a Pre-Listing Inspection

To buyers, these aren’t cosmetic issues. They’re trust issues. And that’s what you need to watch out for today. Once buyers start wondering “what else might be wrong,” it’s hard to recover momentum.

That’s why some agents are even recommending a pre-listing inspection as a sneak peek into what buyers will see on their own inspection. With that insight, you can:

- Fix concerns before you list, or disclose issues upfront

- Avoid having to respond or negotiate under pressure

- Stop scrambling to find contractors with availability before your closing date

But remember, you don’t have to fix everything. You just have to be strategic about what you do tackle, so you and your buyer aren’t caught off guard.

And that’s why you need an agent who can:

- Decide if a pre-listing inspection is worth it where you live

- Recommend a trusted inspector (if you decide to get one)

- Look at the results with you to identify true dealbreakers in your market

- Help you decide what to fix or what to credit

- Make sure you avoid over-spending or under-preparing

Bottom Line

One of the biggest dealbreakers for buyers today is inspection issues – and that’s something you can control. You just need to be proactive about high-impact repairs before you list.

If you want help figuring out where to focus, let’s connect so we can keep your sale on track from day one.

Spring Sellers Have the Edge: Why Homes Sell Faster and for More in the Spring Market

Spring Sellers Have an Edge. Here’s Why.

Most homeowners thinking about selling want the same three things:

-

Plenty of interested buyers

-

Strong offers

-

And a quick sale

The good news? Spring is the season most likely to deliver all three.

Across Massachusetts—and especially in communities like Walpole, Dedham, Westwood, and West Roxbury—the spring market consistently brings increased buyer activity. Families want to move before the next school year, the weather improves for house hunting, and many buyers who paused their search during winter suddenly reappear.

If you’ve been thinking about selling your home this year, spring is when momentum tends to swing in your favor.

Let’s take a look at why.

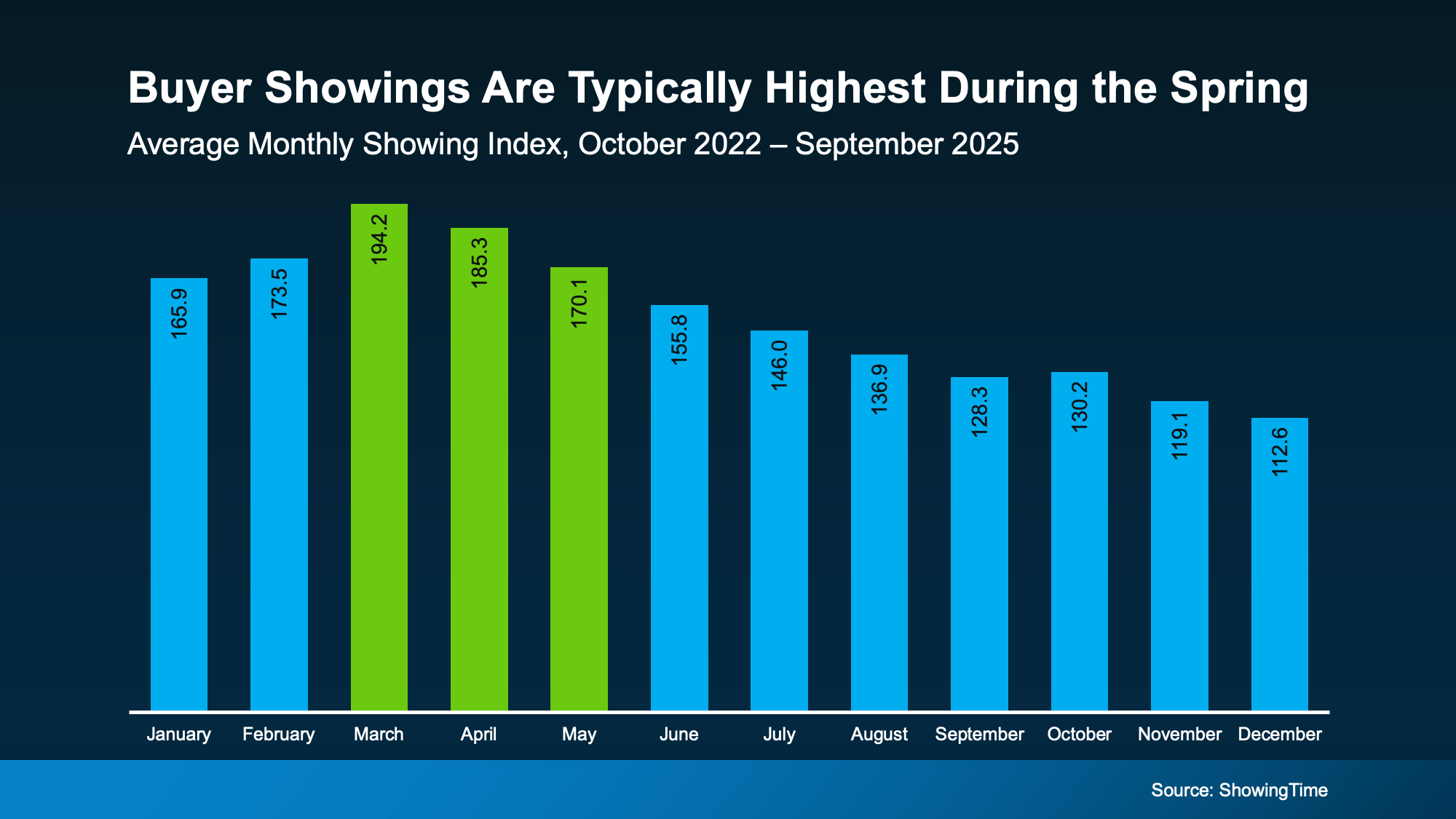

1. More Buyers Are Actively Looking

The housing market has a rhythm to it. And historically, spring is when buyer activity peaks.

Data from ShowingTime consistently shows the highest buyer showing activity occurring between March and May each year.

That means more:

-

online searches

-

showing requests

-

open house visitors

-

and serious buyers entering the market

This year there’s another factor helping sellers too: mortgage rates have recently dropped to near three-year lows.

When affordability improves even slightly, buyers who were sitting on the sidelines often jump back into the market.

More buyers + improved affordability = more people walking through your front door.

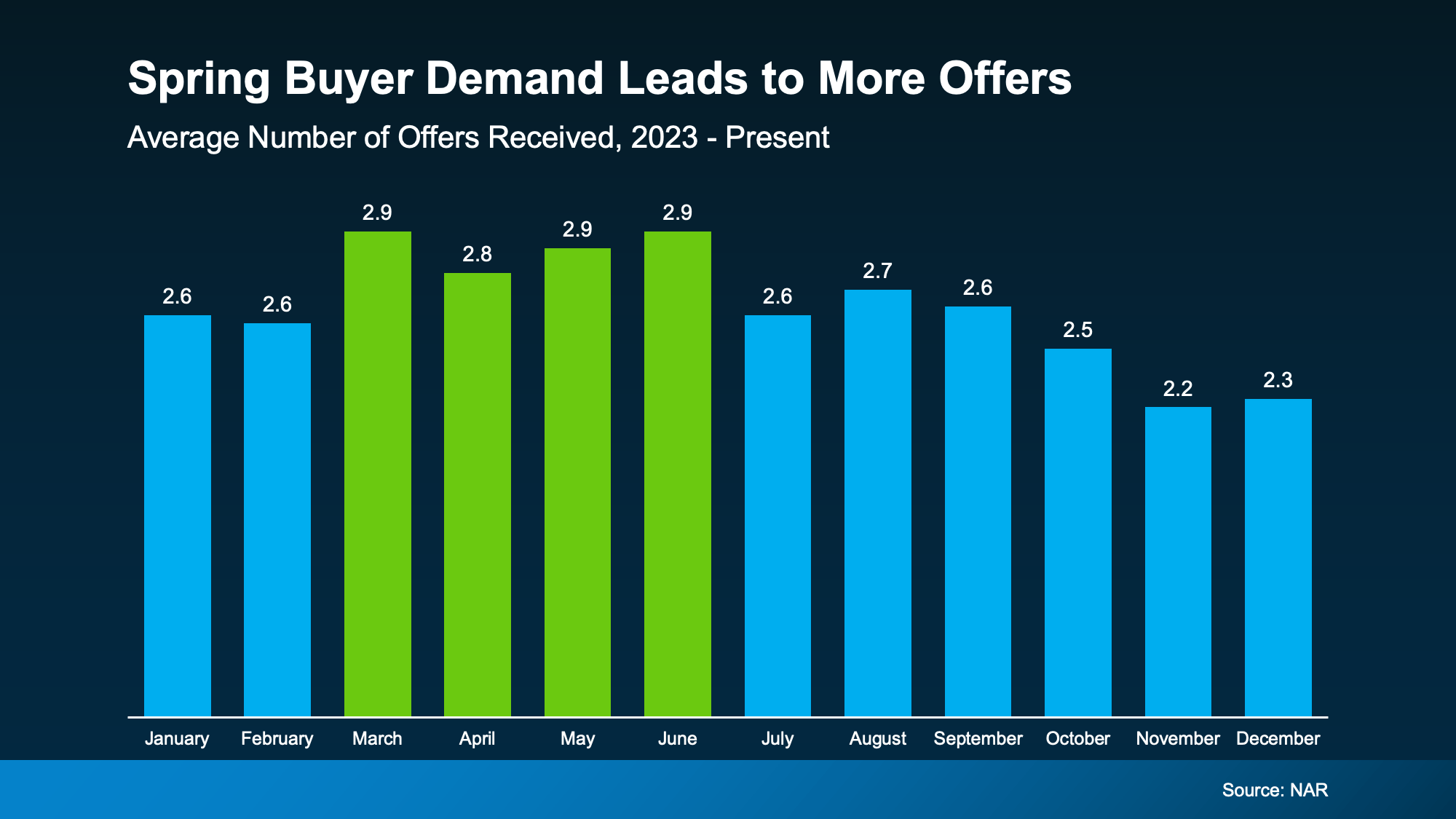

2. Spring Homes Often Receive More Offers

More buyers naturally leads to more competition for well-priced homes.

According to data from the National Association of Realtors, homes listed in the spring typically receive more offers on average than during winter months.

Why?

Because buyers often feel a little urgency in spring.

Many want to:

-

move before summer

-

close before the next school year

-

or secure a home before competition grows

Now, let’s be realistic.

We’re not seeing the wild bidding wars of 2020–2021 where buyers were offering $100K over asking and naming their firstborn after the seller.

But spring still tends to bring the strongest buyer demand of the year, and that competition can work in a seller’s favor.

More offers can mean:

-

stronger pricing

-

fewer contingencies

-

and better negotiation power

Not a bad position to be in.

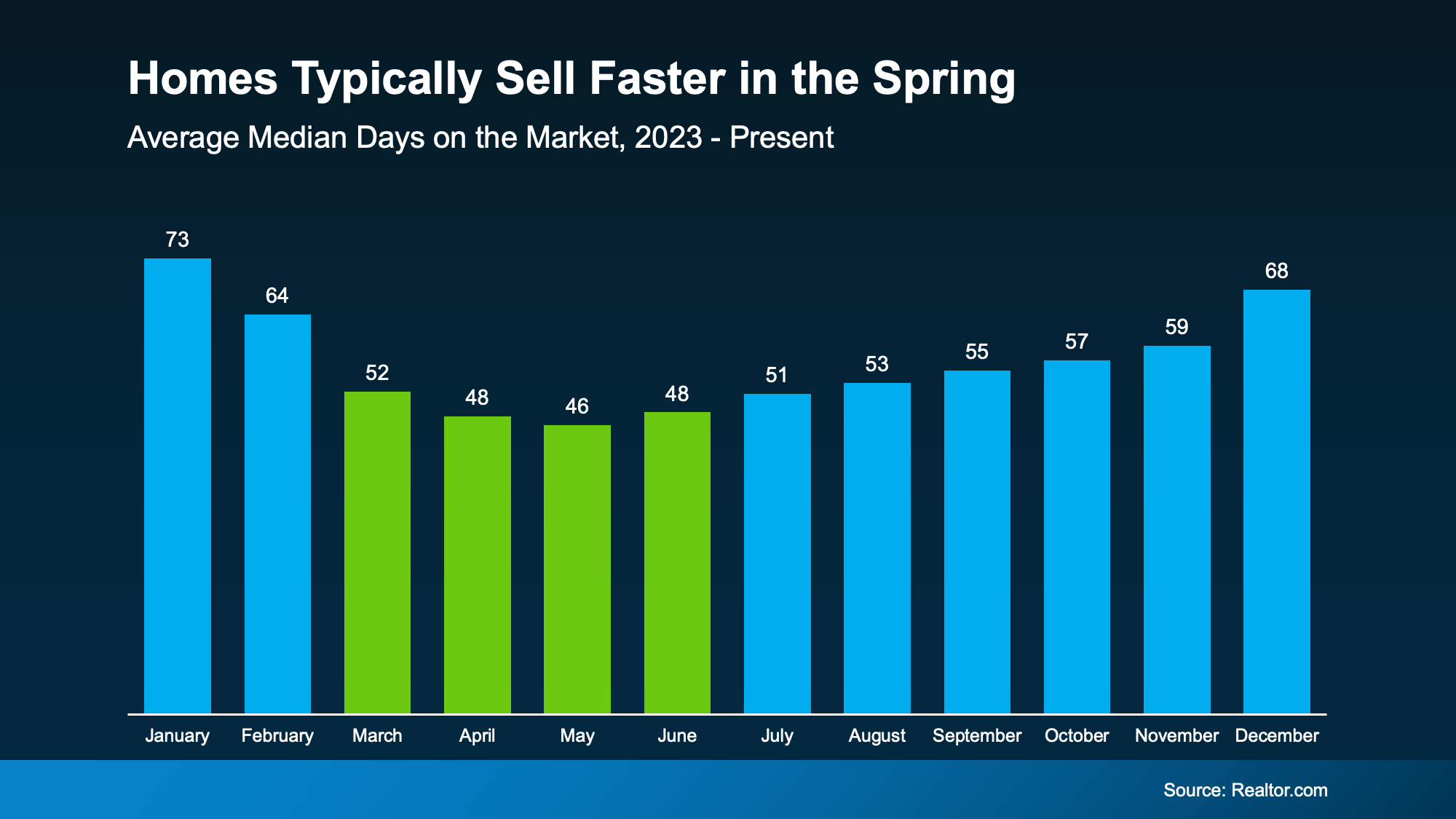

3. Homes Typically Sell Faster in Spring

Another seasonal trend? Homes move quicker.

According to Realtor.com data, homes listed in spring typically sell about 20 days faster than homes listed in winter.

That’s nearly three weeks shaved off the selling timeline.

For sellers, that matters.

A faster sale means:

-

less disruption to daily life

-

fewer weeks of keeping the house showing-ready

-

quicker access to your equity

-

and the ability to move on to your next chapter sooner

In local markets like Walpole, Dedham, Westwood, Norfolk, Wrentham, and Roslindale, where inventory can already be limited, increased spring demand can make that timeline even shorter.

Why This Matters for Massachusetts Sellers

Massachusetts markets tend to amplify seasonal trends.

Winter in New England can slow activity down—snow, cold weather, and holidays often pause the housing search.

Then spring arrives and suddenly:

-

buyers who waited through winter reappear

-

new buyers enter the market

-

and sellers who prepared during winter finally list

That surge in activity is why spring listings often perform better.

And if inventory remains limited—which is still the case in many Greater Boston communities—sellers may have even more leverage.

Is Spring the Right Time for You to Sell?

Spring doesn’t guarantee a perfect sale.

Strategy still matters.

Pricing correctly, preparing your home, and marketing it effectively are what truly determine the outcome.

But listing during the most active season of the year gives sellers something incredibly valuable:

Momentum.

More buyers.

More activity.

More opportunity.

Bottom Line

If you’re planning to sell your home this year, spring may give you the biggest advantage.

Buyer demand rises.

Offers tend to increase.

And homes usually sell faster.

The real question becomes simple:

If you’re going to sell this year, why not do it when the odds are in your favor?

If you’re thinking about selling in Walpole, Dedham, Westwood, Norfolk, Wrentham, Roslindale, or West Roxbury, I’d be happy to show you what the current spring market looks like for your home.

Get your free home valuation today and see what your home could sell for in today’s market.